Mongolian Meat Prices, Seven Years Later

In 2019 I wrote about Mongolia's meat prices and made some predictions. Seven years of new data later, let's see what happened.

In 2019 I predicted meat prices would drop. They did. Then things got complicated.

Back in May 2019 I wrote about Mongolia’s meat prices, dug into the data on exports, animal losses, and inflation, and even made some forecasts about my predictions on meat prices going forward. At the time beef was 10,904 MNT per kilogram in Ulaanbaatar and mutton was 9,777 MNT. I argued that exports weren’t the main price driver, that animal losses were, and that meat was actually getting more affordable relative to wages.

Seven years is a long time. Since then we’ve had a global pandemic, border closures with China, and the worst dzud since 2010. I wanted to revisit the original analysis with fresh data from the National Statistics Office and see what held up and what didn’t.

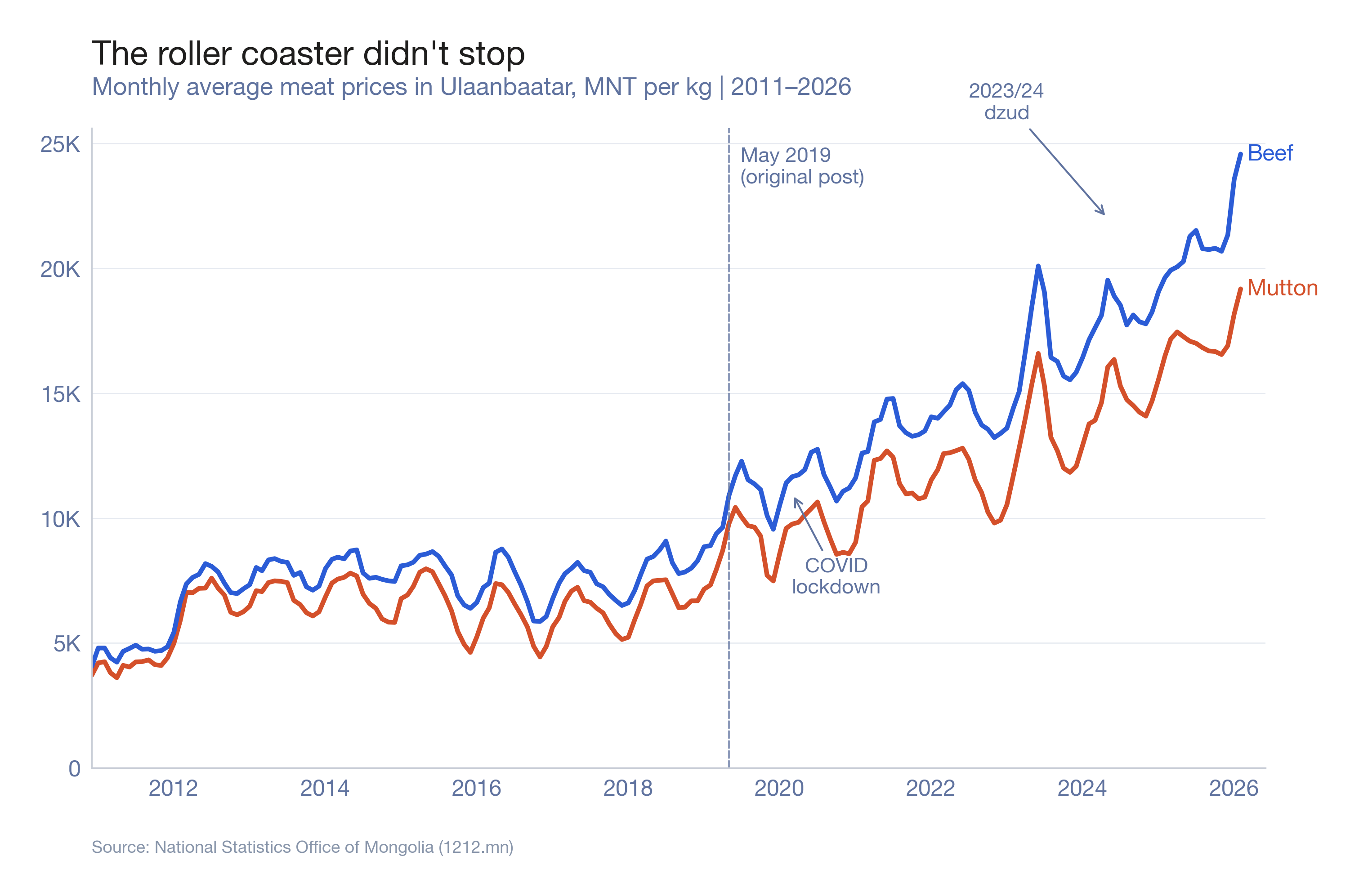

The roller coaster didn’t stop

As of February 2026, beef in Ulaanbaatar costs 24,581 MNT per kilogram. Mutton is 19,181 MNT. That’s an increase of 125% for beef and 96% for mutton since May 2019.

But the path there wasn’t a straight line. After I published the original post, prices did come down through the summer of 2019 (my forecast actually got that right). Then COVID hit in early 2020. Mongolia closed its borders, including with China, and exports dropped. Prices stayed relatively flat through 2020 and into 2021.

The real acceleration started in 2022. A combination of post-COVID inflation, rising animal losses, and a weakening tugrik pushed prices up fast. By 2023 both beef and mutton were roughly double their 2019 levels. And then the dzud hit.

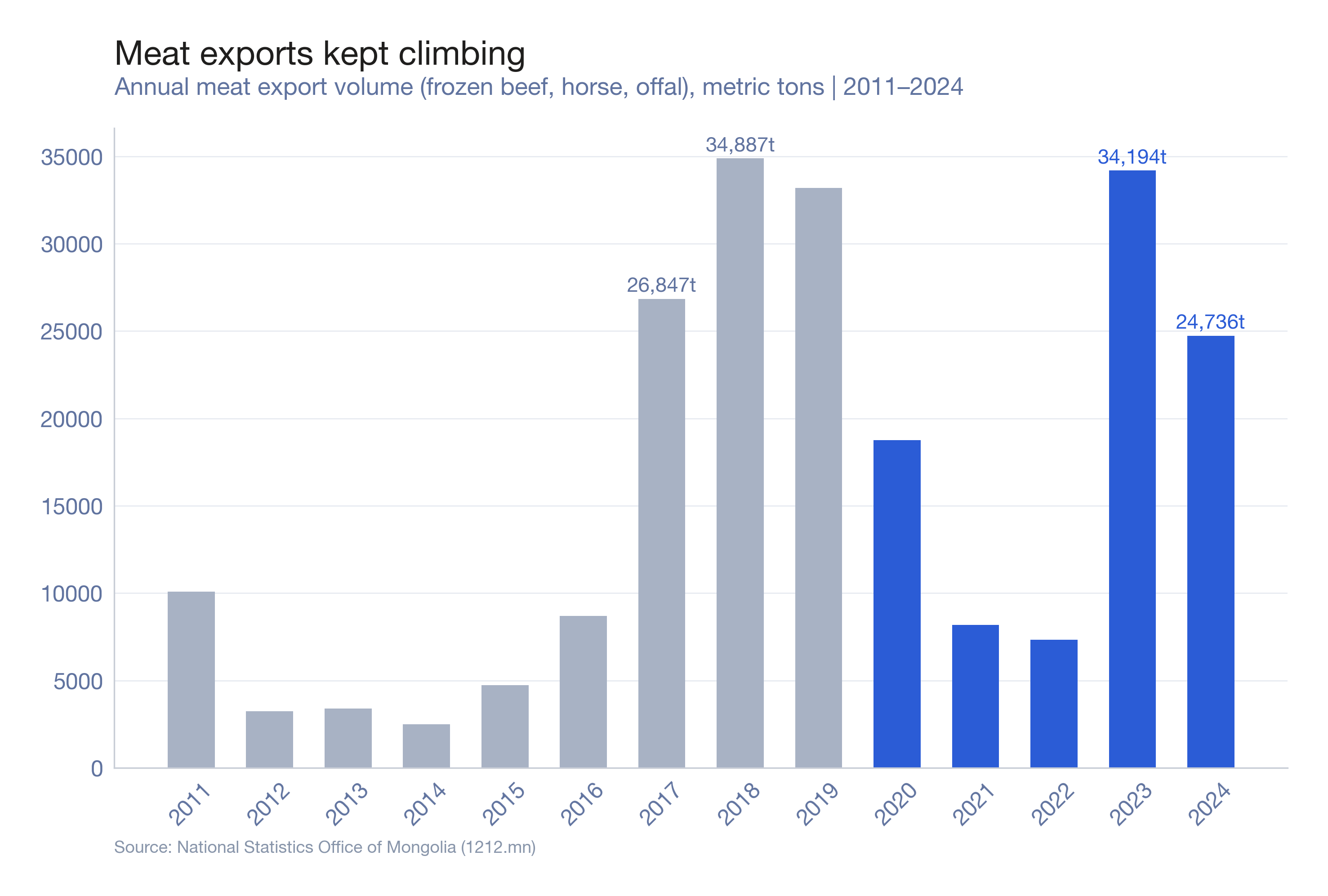

Exports: still not the main driver

In the original post I argued that meat exports weren’t the primary driver of prices. The data since 2019 only makes that case stronger.

COVID cratered exports. In 2020 meat exports dropped to 18,769 tons from 33,193 in 2019. In 2021 and 2022 they stayed below 10,000 tons. Yet prices kept climbing.

Then exports bounced back in 2023 to 34,194 tons (nearly matching the 2018 peak of 34,887 tons) and fell again to 24,736 tons in 2024. The correlation between exports and prices remains weak. Prices went up when exports dropped. Prices went up when exports rose. The relationship just isn’t there.

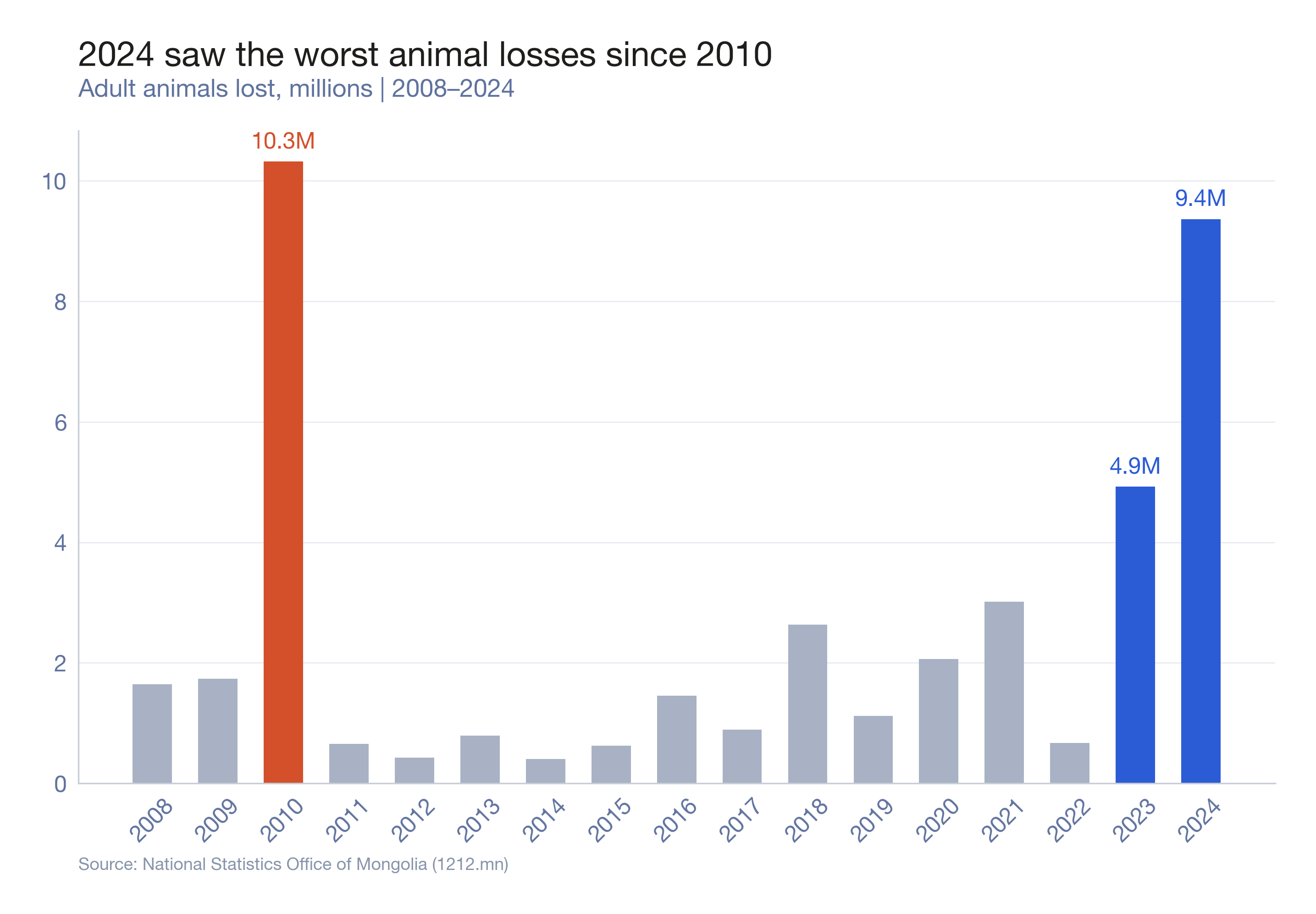

The dzud came back

This is the big story. In 2024, Mongolia lost 9.4 million adult animals. That’s the worst year since 2010’s devastating dzud when 10.3 million died.

But 2024 didn’t come out of nowhere. Animal losses had been creeping up for years: 2.6 million in 2018, 3.0 million in 2021, and then 4.9 million in 2023 before the 9.4 million in 2024. Two consecutive years of heavy losses (14.3 million animals across 2023 and 2024 combined) is something Mongolia hasn’t experienced in recent memory.

The total national herd dropped from about 71 million animals in 2019 to 57.6 million by the end of 2024. That’s a loss of roughly 13 million head in five years, or about 19% of the herd.

Looking back at the original post, I wrote that the 2.6 million animals lost in 2018 was “a very likely explanation for rising prices.” The 2023/24 losses were more than five times that number across two years. The connection between animal losses and prices remains the strongest signal in this data.

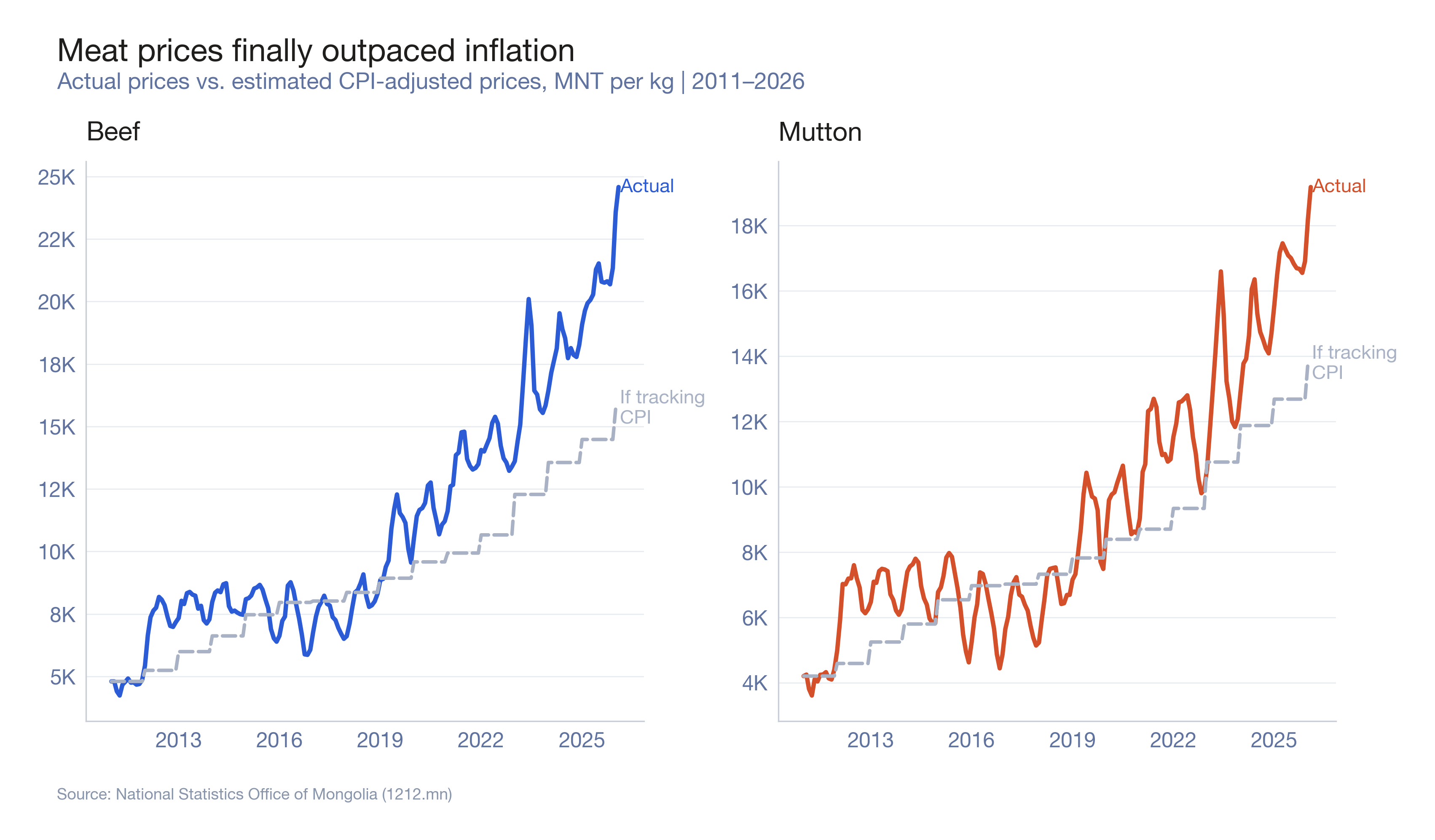

Meat prices finally outpaced inflation

This is where things changed from the original analysis.

In 2019 I showed that meat prices had been remarkably stable relative to inflation since 2011. For years, actual prices tracked below what you’d expect if they simply followed CPI. I interpreted this as meat getting cheaper in real terms.

That story flipped around 2022. Both beef and mutton prices broke above the CPI trendline and haven’t come back. Beef at 24,581 MNT is well above the 14,000 or so MNT you’d expect from CPI alone. Mutton tells a similar story.

The combination of back-to-back dzuds, post-COVID inflation (13.8% in 2021, 13.2% in 2022), and a weakening currency appears to have broken the pattern. Meat prices are now outpacing inflation.

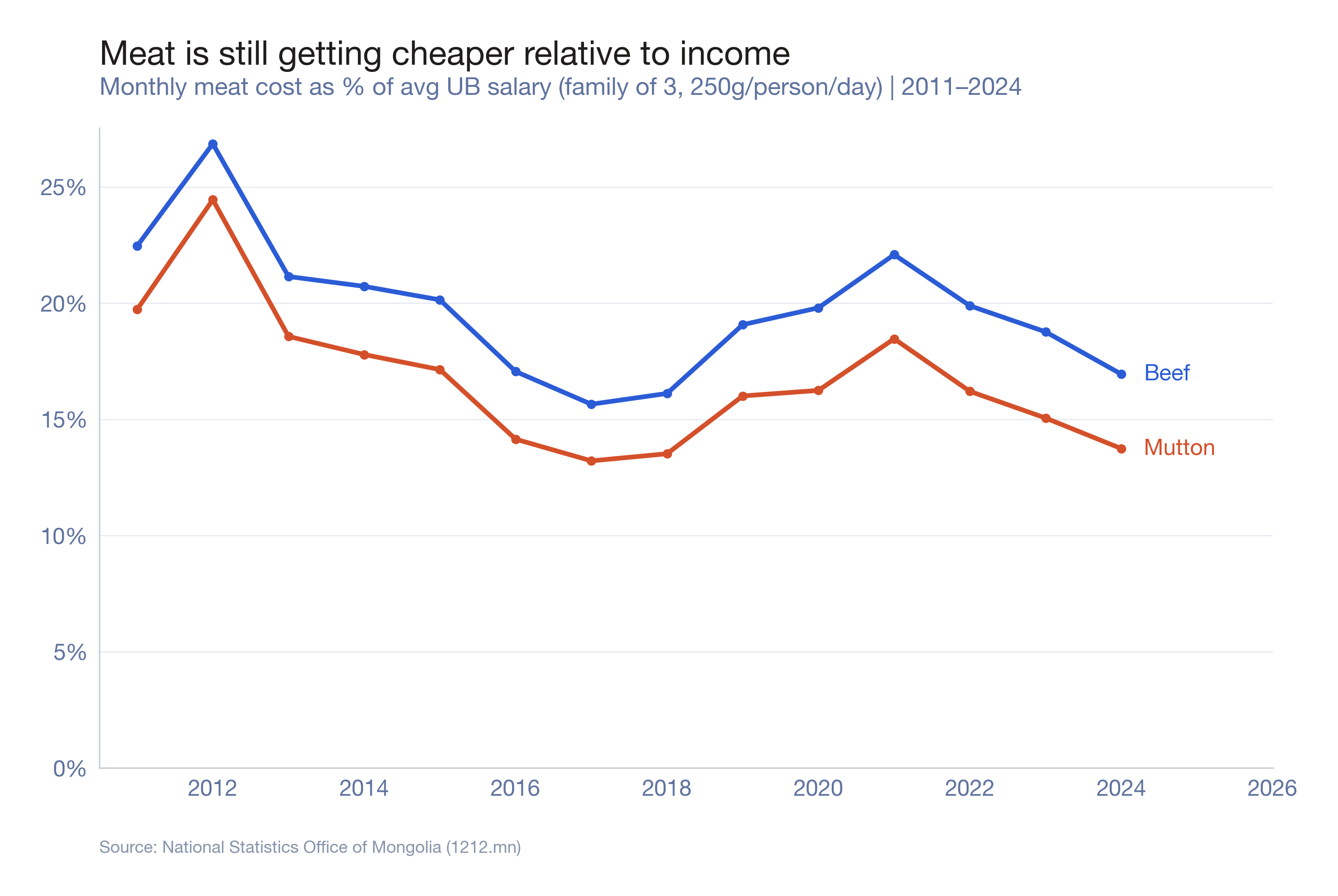

Are Mongolians still spending less on meat?

Despite the price increases, the answer is still mostly yes.

I used the same methodology from the original post: a family of three in Ulaanbaatar, each person eating 250 grams of meat per day (roughly in line with average US consumption), earning the average UB salary.

In 2011 that family would have spent about 22.5% of their income on beef (or 19.7% on mutton). By 2019 it was 19.1% for beef and 16.0% for mutton. In 2024: 16.9% for beef and 13.7% for mutton.

The trend held. Wages in Ulaanbaatar have grown faster than meat prices. The average monthly wage went from 470,300 MNT in 2011 to 2,390,700 MNT in 2024, an increase of over 400%. Beef prices increased about 300% over the same period.

There was a noticeable bump in 2022 when wages hadn’t caught up with the post-COVID price spike, but by 2024 the long-term downward trend had reasserted itself. For the average UB household, meat consumes a smaller share of income than it did a decade ago.

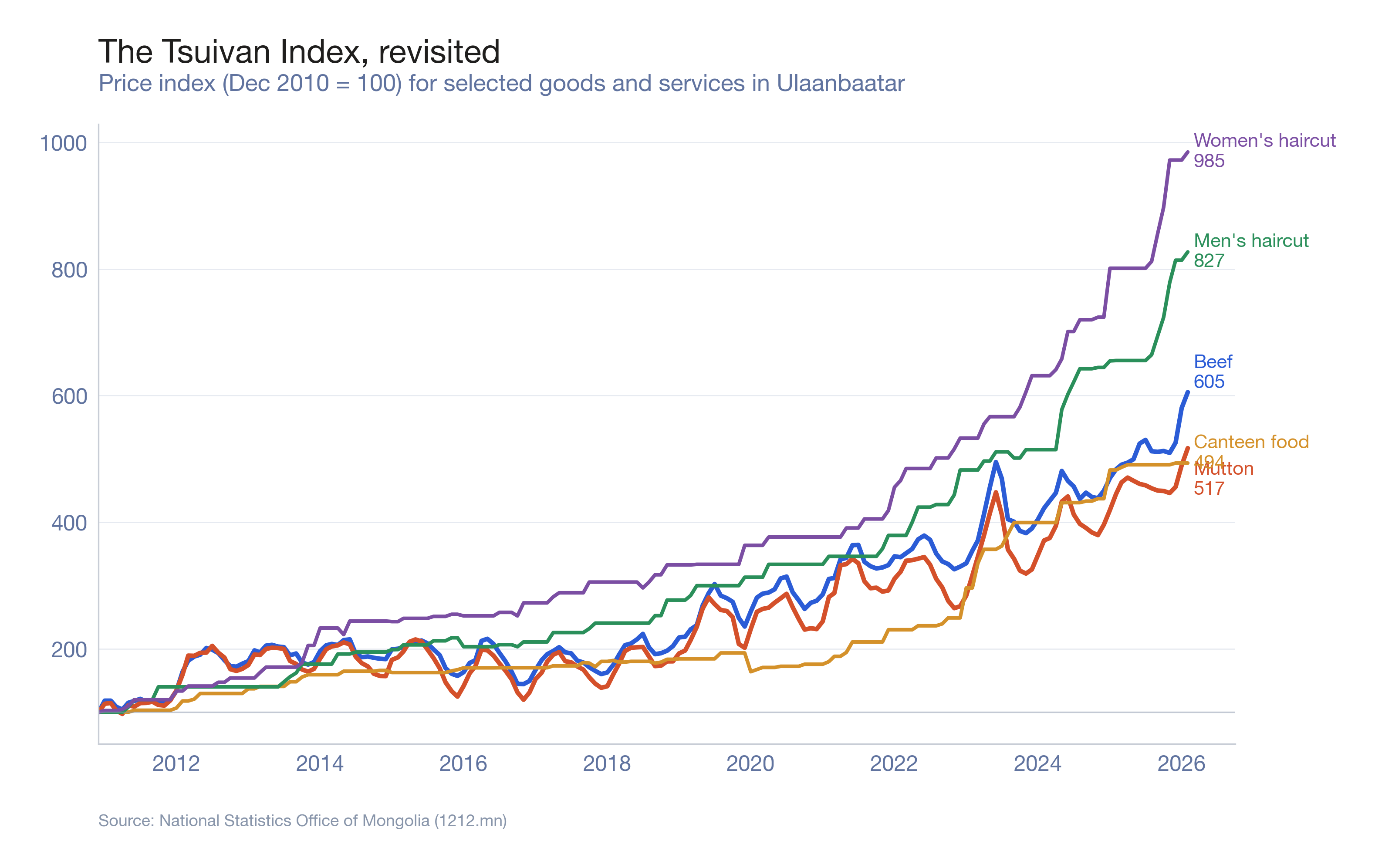

The Tsuivan Index, revisited

This was a reader favorite from the original post. I created a price index using December 2010 as the base (100) for several common goods and services tracked by the NSO.

The results are pretty wild. Women’s haircuts have increased 885% since December 2010 (index of 985). Men’s haircuts are up 727% (index of 827). Both have far outpaced beef (505%, index of 605) and mutton (417%, index of 517). Canteen food (the NSO’s current category closest to tsuivan) sits at 494.

In the original post I noted that haircuts were the most surprising price increase. Seven more years of data just made that gap wider. Haircuts continue to outpace everything else in this basket by a large margin. This makes some intuitive sense: haircuts are pure labor, and labor costs in Ulaanbaatar have been growing fast. You can’t import a cheaper haircut from China.

What I got right and what I got wrong

Right: My forecast predicted prices would drop after the spring 2019 peak. They did. Animal losses remain the strongest predictor of price movements. Exports still don’t correlate well with prices. Meat has continued to get more affordable as a share of income.

Wrong (or at least different now): The inflation comparison reversed. In 2019, meat prices tracked below CPI. By 2026 they’re well above it. The 2023/24 dzud was a supply shock large enough to break the pattern that had held for a decade.

The question I raised in the original post about government reserve meat remains as relevant as ever. With 14.3 million animals lost across 2023 and 2024, the pressure on herders and on consumer prices is real. Whether the government’s reserve meat program can meaningfully buffer against shocks of this scale is still not clear from the available data.

All data in this post comes from Mongolia’s National Statistics Office (1212.mn).